Derivation of the Least Squares Estimator for Beta in Matrix Notation – Proof Nr. 1 | Economic Theory Blog

Excerpt

In the post that derives the least squares estimator, we make use of the following statement: latex \frac =2X’Xb&s=2 This post shows how one can…

In the post that derives the least squares estimator, we make use of the following statement:

This post shows how one can prove this statement. Let’s start from the statement that we want to prove:

Note that

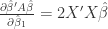

Let’s compute the partial derivative of

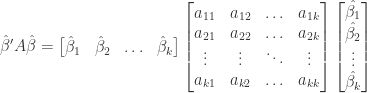

Instead of stating every single equation, one can state the same using the more compact matrix notation:

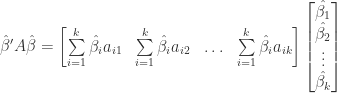

plugging in

Now let’s return to the derivation of the least squares estimator.